March 31, 2026

Banking Jobs at Risk: Inside the Rise of AI and Automation

Dr. Tanvir Hussein

A weekly stock market roundup covering global, GCC, and Bahrain markets, highlighting key trends, oil price movements, geopolitical risks, and investor sentiment.

FinTake Weekly Market Wrap | Week ending April 3, 2026

This week delivered a tale of two markets. While global indices staged a notable rebound from recent lows, the GCC region painted a more complex picture, with diverging performances across individual exchanges. Bahrain, in particular, adopted a defensive posture as investors navigated a confluence of macroeconomic uncertainties and energy market pressures.

Global equity markets bounced back this week, recovering a portion of the losses accumulated over the previous fortnight. The S&P 500 posted modest gains as investor sentiment improved on the back of better-than-expected manufacturing data and easing concerns about an imminent recession. European markets followed suit, with the FTSE 100 and DAX both registering positive weekly closes.

However, the rebound was tempered by persistent uncertainty surrounding trade policy, with markets remaining highly sensitive to any developments on the tariff front. Asian markets were mixed, with Japan’s Nikkei advancing while Chinese indices remained under pressure amid ongoing property sector concerns.

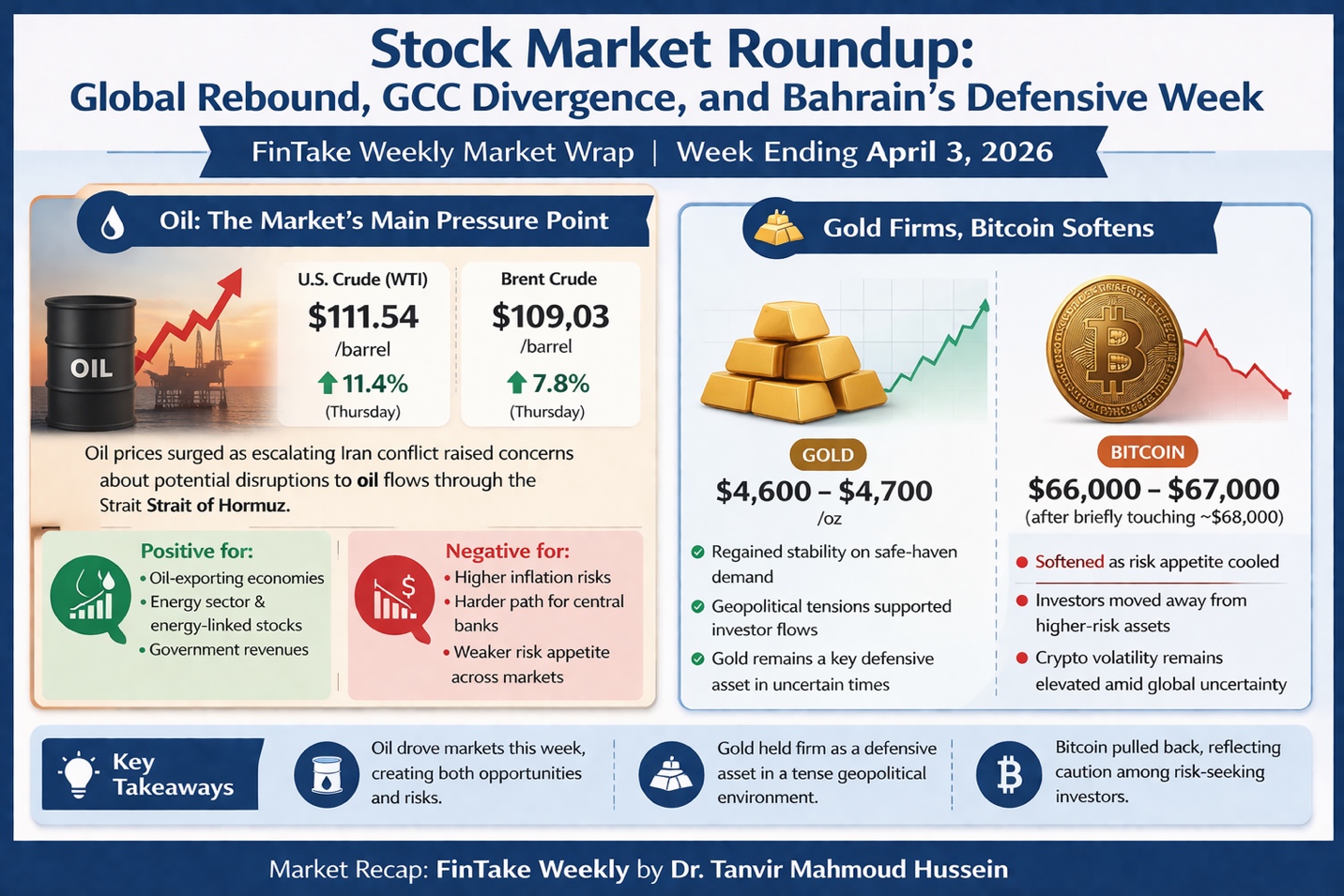

Energy markets remained the dominant force shaping investor sentiment across the GCC. US crude settled at $111.54 per barrel while Brent crude closed at $109.03, reflecting continued supply concerns amid geopolitical tensions in key producing regions. The elevated oil prices present a double-edged sword for the Gulf: supporting government revenues but also fueling inflationary pressures that complicate monetary policy.

OPEC+ production decisions continue to be closely watched, with any signals of output adjustments capable of moving markets significantly. The interplay between geopolitical risk premiums and actual supply-demand fundamentals remains the critical dynamic to monitor.

Gold maintained its position near recent highs as investors sought traditional safe haven assets amid ongoing uncertainty. The precious metal continues to benefit from a combination of geopolitical risk, inflation concerns, and expectations of eventual monetary easing. Bitcoin, meanwhile, showed increased correlation with risk assets, fluctuating in tandem with equity market sentiment rather than acting as the “digital gold” some proponents suggest.

The GCC markets told a story of divergence this week. Saudi Arabia’s Tadawul held relatively steady, closing near 11,268, supported by robust petrochemical earnings and continued domestic investment momentum. Qatar’s exchange adopted a cautious tone, with trading volumes below average as investors awaited clarity on regional economic developments.

The UAE markets experienced the most notable turbulence, with combined losses estimated at approximately $120 billion in market capitalization over recent weeks, driven by concerns over real estate valuations, tightening liquidity, and global risk aversion. The correction has raised questions about whether current levels represent a buying opportunity or signal deeper structural concerns.

The Bahrain Bourse adopted a distinctly defensive posture this week. The market registered a cumulative decline of 7.8% for March, with banking and financial services stocks bearing the brunt of the selling pressure. Trading volumes remained thin, suggesting that institutional investors are sitting on the sidelines awaiting greater clarity on interest rate trajectories and regional economic prospects.

The defensive positioning reflects broader investor caution rather than any specific deterioration in corporate fundamentals. Most listed companies continue to report adequate earnings, and the Central Bank of Bahrain’s regulatory environment remains supportive of market stability.

Three factors dominated market movements this week. Geopolitics remained the overarching concern, with trade tensions, regional conflicts, and diplomatic developments creating persistent uncertainty. Energy prices continued to exert outsized influence on GCC markets, with every dollar move in crude prices translating into significant shifts in market sentiment. Interest rate expectations evolved throughout the week as economic data releases alternately supported and undermined the case for near-term monetary easing.

This week’s market action reinforces several important themes for investors. The global rebound, while welcome, should not be mistaken for a resolution of the underlying uncertainties driving volatility. GCC markets continue to be heavily influenced by oil dynamics, and Bahrain’s defensive positioning suggests that smart money is prioritizing capital preservation over aggressive positioning.

A rebound is not a resolution. Until the underlying drivers of uncertainty—trade policy, geopolitics, and monetary direction—find clearer footing, volatility will remain the market’s default setting.

Dr. Tanvir Hussein

FinTake Weekly Market Wrap | Week ending April 3, 2026

Last Updated: 09 Apr 2026