May 8, 2026

FinTake Weekly Market Wrap: AI & Tech Lead US Markets to Record Highs

Dr. Tanvir Hussein

Explore this week’s global market wrap from Gulf University covering oil prices above $100, Treasury yield pressure, GCC market trends, Bahrain Bourse performance, and AI-driven equities.

Global investors faced another turbulent week as oil prices surged past $100 per barrel, Treasury yields climbed higher, and technology stocks lost momentum after weeks of AI-driven gains.

In this weekly market wrap, we examine how global equities, GCC markets, Bahrain Bourse performance, commodities, and cryptocurrencies reacted to shifting macroeconomic conditions during the week ending May 15, 2026.

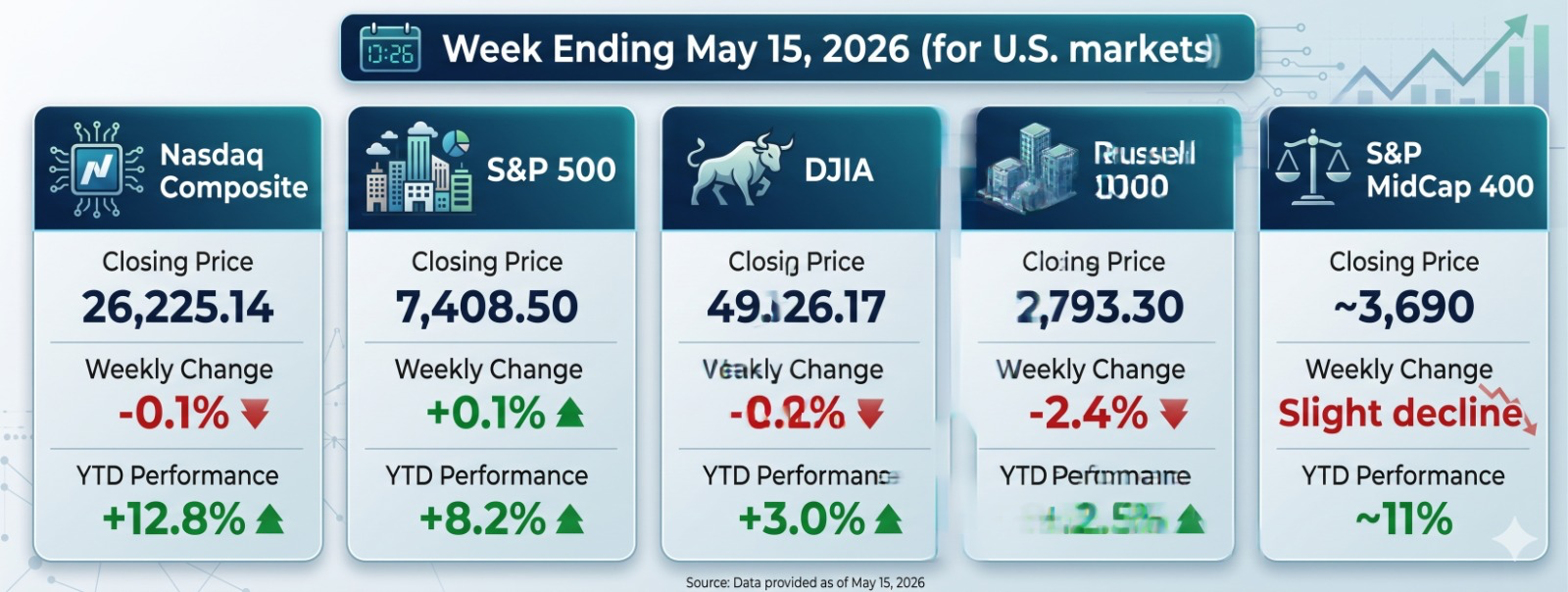

| Index | Friday’s Close | Week’s Change | % Change YTD |

|---|---|---|---|

| Nasdaq Composite | 26,225.14 | -0.1% | +12.8% |

| S&P 500 | 7,408.50 | +0.1% | +8.2% |

| DJIA | 49,526.17 | -0.2% | +3.0% |

| Russell 2000 | 2,793.30 | -2.4% | +12.5% |

| S&P MidCap 400 | 3,690 | Slight decline | 11% |

Source: AP News, Reuters, and market data compiled by FinTake. This table is for illustrative purposes only. Past performance cannot guarantee future results.

U.S. markets were mostly flat to lower for the week ending May 15. The Nasdaq Composite and DJIA posted slight weekly declines, while the S&P 500 edged up marginally. Small-cap stocks, represented by the Russell 2000, saw the sharpest weekly drop at -2.4%. Despite mixed weekly performance, all major indexes remained positive year-to-date, with the Nasdaq and Russell 2000 leading gains. The S&P MidCap 400 also showed modest YTD growth despite a slight weekly decline.

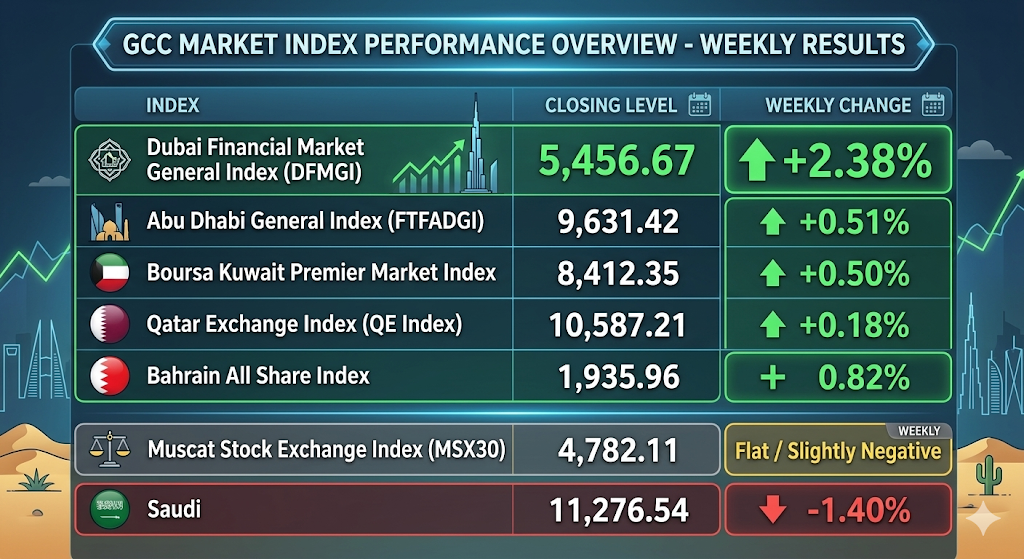

GCC equity markets delivered mixed but relatively resilient performance during the week as investors balanced the positive impact of higher oil prices against rising geopolitical tensions and global monetary-policy uncertainty. Dubai led regional gains, with the DFM General Index rising 2.38% to close at 5,456.67, supported by strong banking and real estate activity. Abu Dhabi and Kuwait posted modest gains, while Qatar remained relatively stable. In contrast, Saudi Arabia’s Tadawul Index declined 1.40% amid cautious investor sentiment and profit-taking activity.

Regional markets remained sensitive to developments surrounding Middle East tensions and shipping risks near the Strait of Hormuz, while investor positioning continued to favor banking, telecom, energy, and infrastructure-linked sectors over broad-based equity buying.

Investor flows across GCC exchanges remained selective, with stronger positioning in banking, telecom, energy, and infrastructure-linked companies rather than broad-based equity buying.

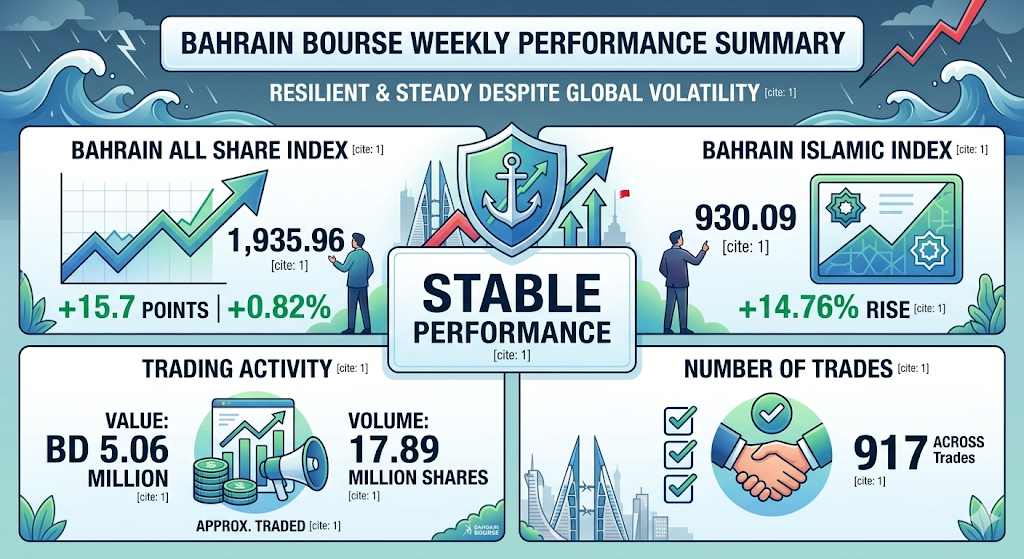

Despite increased global volatility, Bahrain Bourse maintained a relatively stable and defensive performance during the week. The Bahrain All Share Index closed at 1,935.96, gaining 15.7 points (+0.82%), while the Bahrain Islamic Index rose to 930.09, up 14.76% for the week. Total traded value reached approximately BD 5.06 million, with trading volume of 17.89 million shares across 917 trades.

Investor activity remained concentrated in banking, investment, and selected real estate stocks, with GFH Financial Group, Salam Bank, BBK, and SEEF among the most actively traded securities. Meanwhile, SEEF Holding, Esterad, and BISB led weekly gains, reflecting continued selective positioning in defensive sectors amid broader regional and global market uncertainty.

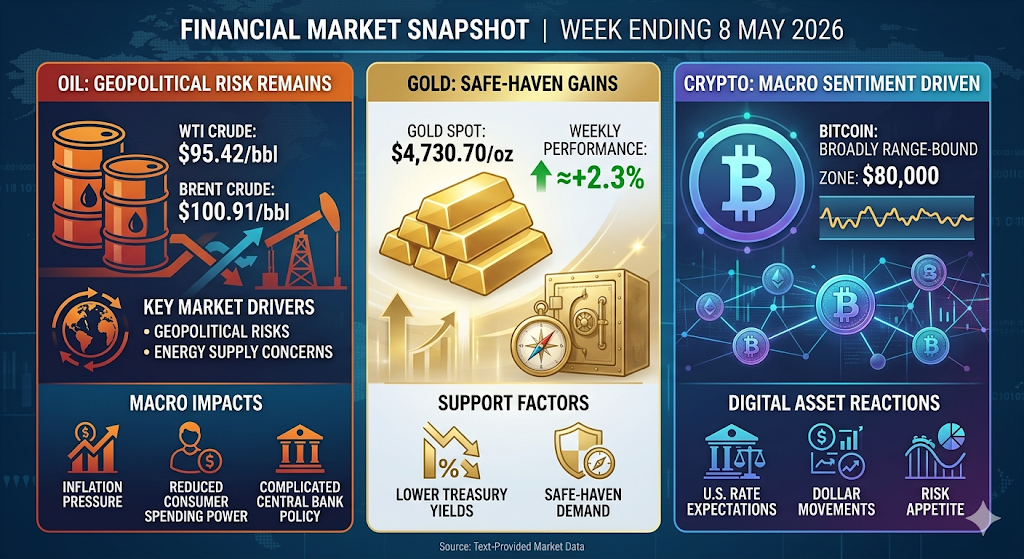

Oil prices rose sharply during the week as geopolitical tensions intensified across the Middle East and concerns grew over possible supply disruptions near the Strait of Hormuz.

Energy markets remained highly sensitive to shipping disruptions and regional conflict risks, with elevated oil prices increasing concerns over global inflation and the future path of central bank interest-rate policies.

Gold prices softened modestly during the week, approximately $4,540–$4,660 per ounce, despite heightened geopolitical uncertainty. Rising U.S. Treasury yields and a firmer U.S. dollar limited investor demand for non-yielding safe-haven assets.

Bitcoin traded broadly within the $78,000–$80,000 range during the week, while overall cryptocurrency markets remained volatile and sentiment-driven.

Digital assets continued to react primarily to macroeconomic developments, interest-rate expectations, and broader risk appetite rather than crypto-specific catalysts.

The week ending 15 May 2026 highlighted the growing influence of geopolitical developments, energy markets, and bond yields on investor sentiment. While long-term optimism surrounding artificial intelligence and technology remains intact, markets are becoming increasingly sensitive to inflation risks, higher financing costs, and global supply concerns.

For GCC markets, elevated oil prices continue to provide underlying support, although geopolitical uncertainty remains a key limitation to stronger market momentum. Bahrain’s steady and stable performance once again reinforced its position as a defensive investment market within the GCC region.

FinTake View: With oil above $100, rising Treasury yields, and a brief pause in the AI rally, investors should stay disciplined — favoring quality earnings, defensive sectors, and selective regional exposure while monitoring inflation, geopolitical risks, and central bank signals.

Disclaimer: This report is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results.

Sources: AP News, Reuters, Bahrain Bourse, Bureau of Labor Statistics, Federal Reserve, Dubai Financial Market, Investing.com, Investrade, Yahoo Finance, Zawya by LSEG.

Dr. Tanvir Mahmoud Hussein

Associate Professor (Finance) — College of Administrative and Financial Science, Gulf University

Last Updated: 15 May 2026