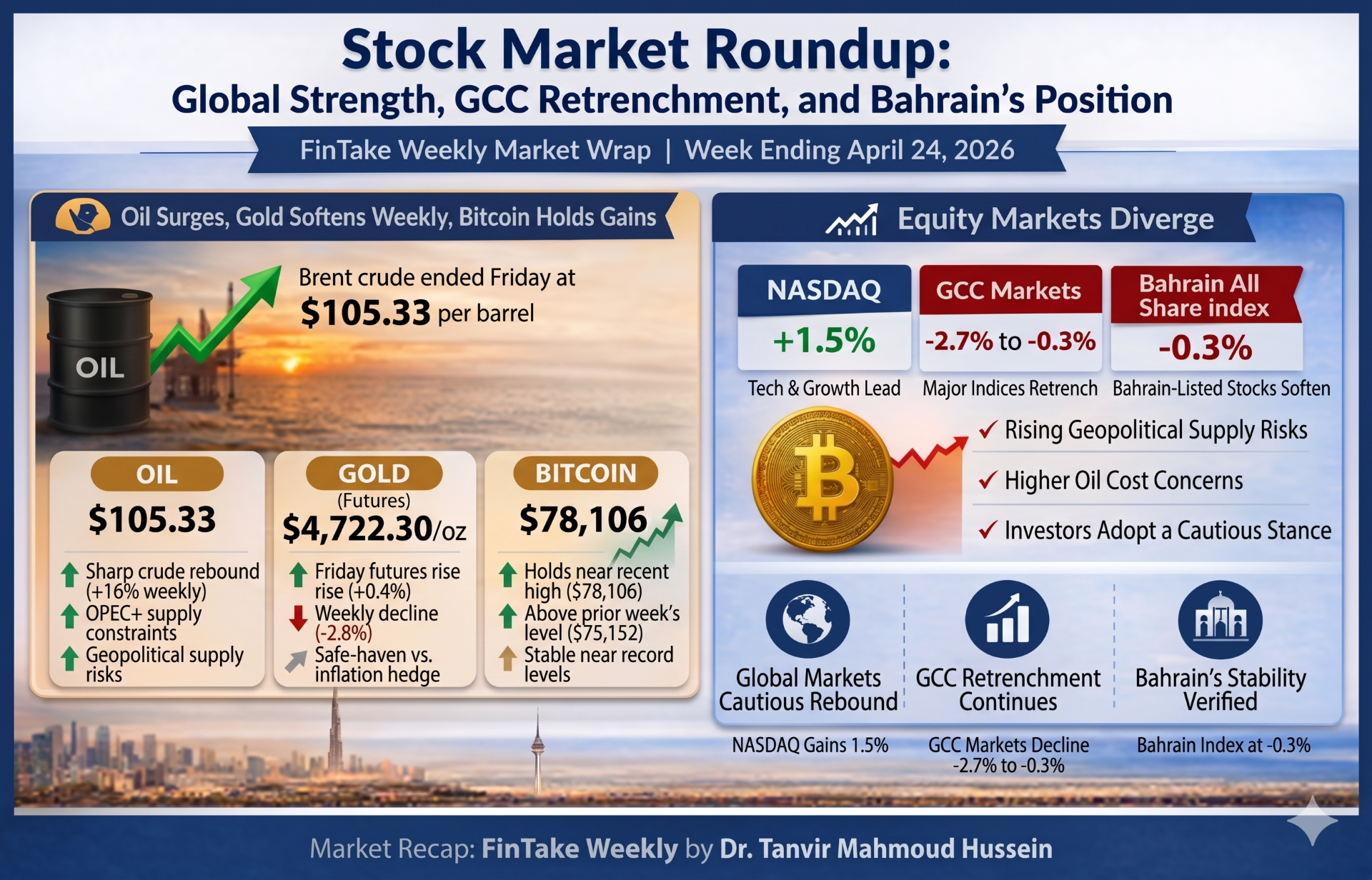

April 24, 2026

Stock Market Roundup: Global Strength, GCC Retrenchment, and Bahrain’s Position

Dr. Tanvir Mahmoud Hussein

A weekly stock market roundup from Gulf University covering global, GCC, and Bahrain markets, with focus on index performance, commodities, earnings, policy signals, and investor sentiment.

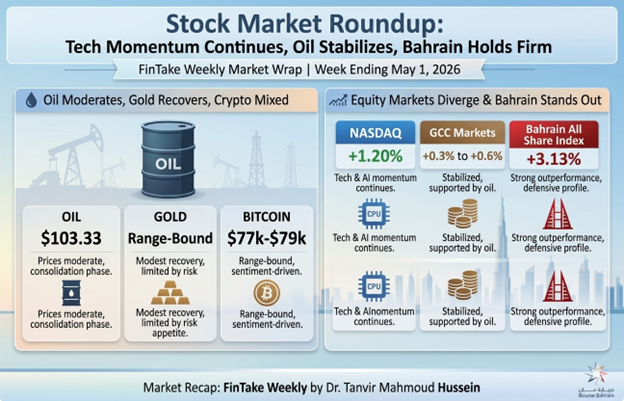

Global equity markets extended their upward trend, though gains remained concentrated in technology and AI-driven stocks. The Nasdaq Composite continued to outperform, supported by sustained investor enthusiasm for semiconductor and artificial intelligence companies. Meanwhile, the S&P 500 posted moderate gains, while the Dow Jones Industrial Average remained relatively flat and the Russell 2000 posted a modest gain of around +0.5%, reflecting continued weakness in smaller-cap segments.

Technology stocks, particularly in AI and chip manufacturing, remained the primary drivers of market momentum. However, cautious sentiment persisted due to uncertainty around interest rate policy and global inflation trends.

| Index | Friday’s Close (1 May) | Week’s Change | % Change YTD |

|---|---|---|---|

| Nasdaq Composite | 25,134.2 | 297.6 | 8.15% |

| S&P 500 | 7,193.6 | 28.52 | 5.08% |

| DJIA | 49,280.1 | 49.39 | 2.53% |

| Russell 2000 | 2,801.5 | 14.5 | 13.10% |

| S&P MidCap 400 | 3,658.2 | 16.88 | 10.65% |

This chart is for illustrative purposes only. Past performance cannot guarantee future results.

GCC markets showed signs of stabilization after the previous week’s declines. Oil price consolidation provided some support, but geopolitical tensions and global monetary uncertainty continued to limit strong upside momentum.

Indicative estimates based on market trends; compiled from multiple sources.

Investor sentiment remained selective, with capital flowing into energy and defensive sectors rather than broad-based equity rallies.

Bahrain delivered a strong weekly performance. According to the Bahrain Bourse’s weekly trading report, the Bahrain All Share Index increased from 1,912.20 to 1,972.05 for the week ending April 30, showing a gain of about 3.13%. Weekly traded volume reached approximately 19.99 million shares, with a total traded value of around BD 5.13 million and 958 trades recorded.

Among individual stocks, GFH emerged as the top gainer with a rise of 13.02%, followed by ESTERAD (+7.69%) and BNH (+7.65%), while SEEF led the losers with a decline of -7.64%, followed by SOLID (-4.42%) and ALBH (-2.65%), reflecting selective investor activity in the market. Overall, the market reflected targeted investor positioning rather than a broad sector-wide rally, while maintaining its relatively stable and defensive profile within the GCC.

Oil prices moderated slightly after the previous week’s sharp rally:

Markets entered a consolidation phase, as immediate supply concerns eased, although geopolitical risks continued to provide underlying support.

Gold posted a modest recovery, supported by safe-haven demand, though overall gains remained limited amid improving risk appetite. Weekly movement remained slightly positive to flat.

Digital assets showed mixed performance, reacting to broader macro trends rather than strong independent momentum.

Three major forces shaped market behavior:

Overall, the week reinforced a market environment driven by concentrated technology strength and cautious global sentiment. While risk appetite remains intact, investors continue to balance growth opportunities with macroeconomic uncertainty, particularly around interest rates and geopolitical developments. Bahrain’s consistent and stable performance highlights its position as a low-volatility market within the GCC, appealing to investors seeking steady returns amid global uncertainty.

The persistence of narrow, technology-led gains suggests that market strength remains fragile and dependent on a limited set of drivers.

Sources: AP news, The Guardian, Qatar News Agency, Trading Economics, Al Jazeera, Zawya/Kamco Invest, and Bahrain Bourse, Bullion rates, Yahoo Finance.

Dr. Tanvir Mahmoud Hussein

College of Administrative and Financial Science — Gulf University

Last Updated: 04 May 2026