June 5, 2026

FinTake Weekly: Markets Retreat, Bitcoin Plunges, and Bahrain Profits Rise

Dr. Tanvir Mahmoud Hussein

FinTake Weekly from Gulf University reviews global, GCC, Bahrain, commodities, and crypto market trends for the week ending July 3, 2026.

The holiday-shortened week of June 29–July 3, 2026, opened the second half of the year on a mixed note. A weaker-than-expected June jobs report supported hopes that the Federal Reserve will hold rates steady, sending the Dow Jones Industrial Average to a fresh record, even as a renewed rotation out of semiconductor and AI-linked names weighed on the Nasdaq and small caps. Oil extended its multi-week decline, while Bitcoin staged a sharp rebound after touching some of its lowest levels of the year. Bahrain’s market gave back a small part of the prior two weeks’ gains amid a resurgence of Iran-related tensions ahead of the funeral of Iran’s late Supreme Leader. Note: U.S. markets were closed on Friday, July 3, in observance of the Independence Day holiday, so all U.S. weekly figures below reflect Thursday, July 2 closing levels, the last trading session of the week.

U.S. equities closed out the holiday-shortened week on a mixed note. On Thursday, July 2, 2026 — the last trading session before the Independence Day holiday — the Dow Jones Industrial Average surged 594.83 points (+1.14%) to a record close of 52,900.07, while the S&P 500 was essentially flat, adding just 0.01 points to 7,483.24. The Nasdaq Composite fell 0.80% to 25,832.67 and the Russell 2000 declined 1.08% to 2,980.05, both dragged lower by a second consecutive day of losses in semiconductor stocks.

The catalyst for the Dow’s record was a June nonfarm payrolls report that came in well below expectations, with the U.S. economy adding just 57,000 jobs versus a consensus forecast of around 115,000, even as the unemployment rate ticked down to 4.2% from 4.3%. The softer print reinforced expectations that the Federal Reserve, under Chair Kevin Warsh, would keep interest rates on hold for the time being. Technology stocks fared worse, however, as investors continued to rotate out of high-flying chip names — Teradyne, KLA, Micron, and Nvidia were all notable decliners — extending a pullback that began earlier in the week. Tesla shares rose despite the broader tech weakness after the company reported second-quarter vehicle deliveries of 480,126, comfortably ahead of analyst expectations. U.S. markets were closed Friday, July 3, for Independence Day.

Figure 1 reflects Thursday, July 2, 2026 closing levels, the last U.S. trading session of the week (U.S. markets were closed Friday, July 3 for the Independence Day holiday). This infographic is for illustrative purposes only and does not represent the performance of any specific security. Past performance cannot guarantee future results.

Large-cap performance diverged sharply from small caps this week. The Dow (+1.97%) and S&P 500 (+1.76%) posted solid gains, and the Nasdaq Composite (+2.11%) also advanced on the week despite Thursday’s pullback, reflecting strength earlier in the period. The Russell 2000, however, declined 1.00% on the week, as the same rotation out of chip and AI-linked names that pressured the Nasdaq on Thursday weighed more heavily on small-cap sentiment.

Most Gulf stock markets closed lower on Thursday, July 2, 2026, after Iran and the United States concluded a further round of indirectly-mediated talks in Doha with no signs of progress toward a lasting peace agreement. Negotiators reportedly spent two days discussing maritime traffic through the Strait of Hormuz and financial incentives for Iran — two pillars of the framework agreement signed in June — rather than the more difficult issues the deal was expected to eventually unlock. Qatar’s Foreign Ministry said the next round of talks would be scheduled only after funeral processions for Iran’s late Supreme Leader, Ayatollah Ali Khamenei, conclude on July 9.

| Country | Index | Close | Change | % Change |

|---|---|---|---|---|

| Saudi Arabia | TASI | 10,853.73 | +1.32 | +0.01% |

| UAE – Dubai | DFMGI | 6,001.93 | -92.05 | -1.51% |

| UAE – Abu Dhabi | FTSE ADX General | 9,885.05 | -56.03 | -0.56% |

| Qatar | QSI | 10,176.15 | -78.45 | -0.77% |

| Kuwait | BKP | 9,164.16 | -9.24 | -0.10% |

| Bahrain | BAX Bahrain | 2,035.66 | -5.94 | -0.29% |

| Oman | MSM 30 Index | 7,581.40 | +14.7 | +0.20% |

Table 1 reflects each market’s closing level as of Thursday, July 2, 2026 (the last trading session of the week for GCC markets), with change measured against the prior week’s close. Sources: Tadawul, DFM, ADX, QE, Boursa Kuwait, and Oman MSX exchange data; Bahrain figures per the Bahrain Bourse Weekly Report. This table is for illustrative purposes only and does not represent the performance of any specific security.

For the week as a whole, performance was mixed and mostly modest. Saudi Arabia’s Tadawul All Share Index ended essentially flat, up 0.01% to 10,853.73. Dubai’s DFM General Index was the weakest performer, down 1.51% to 6,001.93, while Abu Dhabi’s FTSE ADX General Index fell 0.56% to 9,885.05. Qatar’s QE General Index declined 0.77% to 10,176.15, and Kuwait’s Premier Market index eased 0.10% to 9,164.16. Oman’s MSM 30 Index was the week’s best performer among the larger GCC markets, adding 0.20% to 7,581.40. Bahrain’s BAX, as detailed below, slipped 0.29% on the week. On Thursday, July 2 specifically — the session most directly shaped by the inconclusive Doha talks — Saudi Arabia’s index fell 0.3%, weighed by a 1.3% drop in Saudi Arabian Mining Company (Ma’aden); Dubai’s index fell 0.3% on a 2.2% decline in toll operator Salik; and Qatar’s index dropped 0.8%, dragged by a 1.7% fall in Qatar National Bank, the Gulf’s largest lender. Abu Dhabi and Oman each rose 0.2% that day.

Milad Azar, a market analyst at XTB MENA, said continued uncertainty over the talks was likely to keep investors cautious, limiting the chances of a strong near-term recovery.

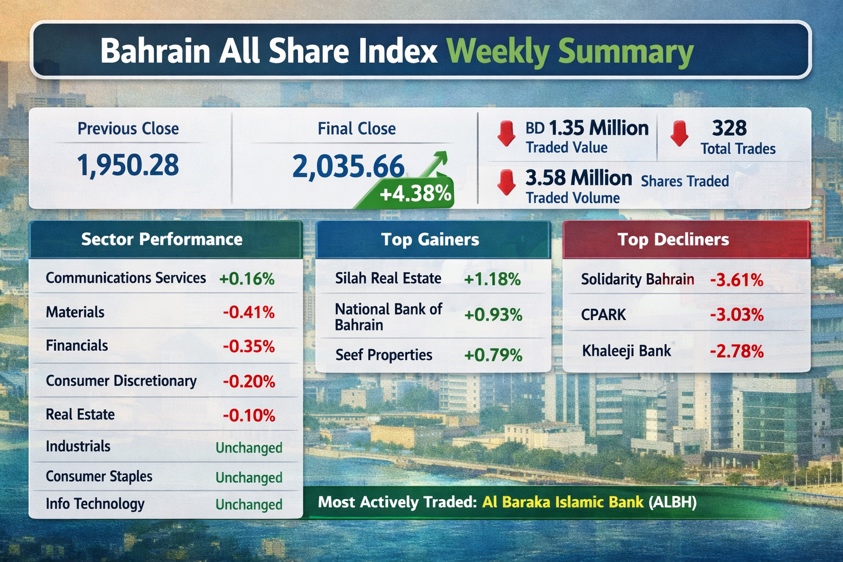

The Bahrain All Share Index (BAX) closed the week ending July 2, 2026, at 2,035.66 points, up from the prior period’s close of 1,950.28 — a rise of about 4.38%. Weekly trading activity eased from the prior week, with traded value down to BD 1.35 million, traded volume down to 3.58 million shares, and the number of trades down to 328.

Sector performance was mixed: Communications Services was the week’s only gainer (+0.16%), while Materials (-0.41%), Financials (-0.35%), Consumer Discretionary (-0.20%), and Real Estate (-0.10%) posted modest declines; Industrials, Consumer Staples, and Information Technology were unchanged. Silah Real Estate (+1.18%), National Bank of Bahrain (+0.93%), and Seef Properties (+0.79%) led the week’s gainers, while Solidarity Bahrain (-3.61%), CPARK (-3.03%), and Khaleeji Bank (-2.78%) were the top decliners; Al Baraka Islamic Bank (ALBH) was the most actively traded name by value.

The market sentiment and stability remained heavily supported by the robust corporate earnings fundamentals recently reported. With total net profits for listed companies climbing 17.6% year-on-year to reach $549.8 million, investor confidence was anchored by key heavyweights. The Materials and Financials sectors provided significant underlying strength, reinforced by exceptional quarterly profit surges from major entities like Alba, alongside solid growth from BBK and GFH Financial Group. Overall, the market demonstrated localized strength and selective buying interest, effectively buffering against the broader global and regional downward pressures.

Oil prices continued to ease this week, extending a decline now stretching back several weeks. Brent crude traded around $71.53 per barrel on the morning of July 2, 2026, down from roughly $73.74 a week earlier — a decline of about 3.0% on the week, as growing confidence in the durability of the Strait of Hormuz reopening continued to weigh on prices.

The renewed uncertainty around U.S.–Iran talks this week introduced some two-way risk to the outlook, though it was not enough to reverse the broader downward trend as physical shipping flows through the Gulf continued to normalize.

Bitcoin rebounded sharply this week after touching some of its lowest levels of the year in the prior period. The cryptocurrency traded around $61,865 on the morning of July 2, 2026, up from roughly $58,981 a week earlier — a gain of about 4.9%, including a single-day jump of more than 6% on July 2 alone.

The rebound came alongside the broader improvement in risk sentiment tied to the softer jobs report and reduced expectations for near-term Fed tightening, though Bitcoin remains well below the highs it touched earlier in the year.

This week reinforced a theme that has run through much of 2026: labor-market data that looks ‘weak’ on the surface can be read by markets as good news, if it supports the case for the Fed to stay on hold. At the same time, the continued rotation out of semiconductor and AI names shows that last year’s most powerful trade remains a source of volatility even amid an otherwise resilient macro backdrop.

FinTake View: With talks now paused around the funeral for Iran’s Supreme Leader, we would watch closely for signs of whether the next round of negotiations restores momentum, or whether markets need to price in a longer period of uncertainty before a fuller resolution is reached.

Disclaimer: This report is for educational and informational purposes only and does not constitute investment advice. Market data reflect the latest available weekly closing figures across each market. Past performance is not indicative of future results.

Sources: Global markets — CNBC, Yahoo Finance, TheStreet, and Zacks Investment Research; Bahrain data — Gulf Daily News (Bahrain Business), citing Bahrain Bourse daily results; Oil & Bitcoin prices — Fortune.

Dr. Tanvir Mahmoud Hussein

Associate Professor (Finance) — Gulf University, Bahrain

Last Updated: 4 Jul 2026